Real estate investors aren’t the only ones concerned about a possible wave of commercial mortgage defaults.

Banks with large percentages of real estate loans are under pressure from regulators to raise money and curb exposure to risky areas of commercial real estate, according to analysts.

“This is a ticking time bomb,” said Gary Findley, an Anaheim-based banking consultant. “We have a lot of local banks that are hugely leveraged with commercial real estate loans.”

During the last decade, many local banks relied on commercial real estate lending as their main profit driver, according to Findley.

“So even if a relatively minor portion of their loans starts having difficulty, it could amount to some significant losses,” he said.

Nationally, $1.4 trillion in commercial mortgages are coming due by 2014. A report by Deutsche Bank AG estimates that 65% of those loans could have trouble refinancing and could default.

In Orange County, nearly $2.7 billion worth of commercial real estate mortgages sold as bonds are expected to come due by 2015 (see story, page 1).

“Commercial real estate is going to be a challenging issue for community bankers in Orange County at least through 2010,” said Ken Cosgrove, chief executive of Anaheim-based Premier Commercial Bank.

A key figure checked by regulators is how much commercial real estate loans a lender has compared to its total capital on a risk-adjusted basis.

Regulators recommend that ratios measuring real estate loans versus total capital don’t exceed 300%.

Of 27 homegrown banks and savings and loans, a dozen are above that percentage based on the latest Federal Deposit Insurance Corp. data from the fourth quarter, according to San Francisco-based investment bank Stone & Youngberg LLC.

But by themselves, real estate loan ratios can be misleading, according to analysts.

Take Costa Mesa-based Pacific Premier Bank, the third-largest bank or thrift based in the county with $802.4 million in assets at year’s end.

Pacific Premier had a real estate loan to capital ratio of 515%. At the same time, it had a capital ratio—measuring the amount of cushion a bank has against loan losses—of 14.55%.

Bank examiners typically consider a 10% capital ratio a minimum, said Michael Natzic, senior vice president of Stone & Youngberg’s community banking group.

“So Pacific Premier is almost 50% more capitalized than the government recommends as minimum levels in this current environment,” he said.

At the same time, the percentage of loans in default or close to default at Pacific Premier was a relatively low 1.74%.

“Even though Pacific Premier seems to have an excessive concentration of (real estate) loans, a broader analysis indicates that this bank clearly has enough capital and its management is attentive to market conditions,” Natzic said.

Pacific Mercantile Bank in Costa Mesa, the largest bank based here with $1.2 billion in assets as of Dec. 31, had a real estate loan to risk-based capital ratio of 264%. It had a capital ratio of 11.29%, or about 13% more than the minimum standard of regulators.

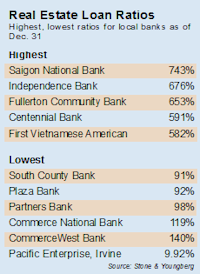

Of the homegrown banks with high real estate loan concentrations, two had capital ratios lower than what regulators like to see. Those were First Vietnamese American Bank and Saigon National Bank, both of Westminster.

First Vietnamese had a real estate loan ratio of 582% and a capital ratio of 7% as of Dec. 31. Nonperforming loans were 20% of its total, by far the greatest of locally headquartered banks and thrifts.

Saigon National had an even higher real estate loan concentration of 743% and a slightly better capital ratio of 8.55%. It had the second-highest nonperforming loans ratio at 14.5%.

The bank has started a second round of raising capital, according to Roy Painter, chief financial officer at Saigon National.

It recently raised $2.5 million, he said.

First Vietnamese also is working on raising money, said Benjamin Palma-Gil, its chief executive. He declined to provide specifics until the process is complete.

Banks here that opened during the later stages of the economic boom are facing many of the same problems, Palma-Gil said.

First Vietnamese entered 2010 with about $57 million in assets. Southern California-based banks coming out of the recession with less than $100 million in assets have faced greater interest expenses than larger competitors, according to Palma-Gil.

“At times like this, capital is king,” he said. “So those with capital are at a competitive advantage in this market. Banks that opened in 2005 are losing money on average.”

First Vietnamese American and Saigon National both opened with fanfare in 2005.